First-time buyers have been the driving force of the housing market for the last decade – supported by Help-to-Buy and greater competition amongst lenders in the 90%+ loan to value (LTV) mortgage market. At the same time, the proportion of sales by existing homeowners has declined.

However, Covid-led market uncertainty combined with the recession and a reliance on higher loan to value mortgages to fund purchases is starting to impact the scale of first-time buyer demand and, moreover, their ability to purchase a home.

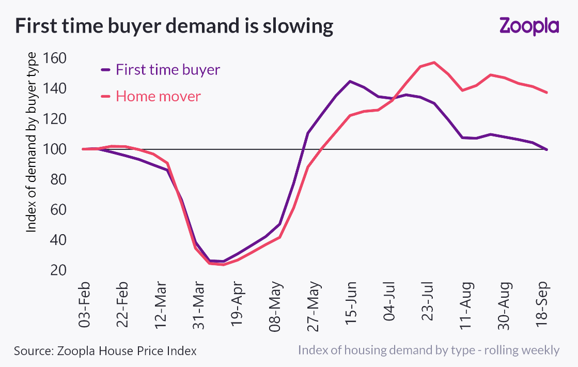

Zoopla figures show that despite a spike in demand amongst first-time buyers when the English housing market reopened after a 50 day closure on 13th May, demand has trended downwards over the last two months and is now back in line with pre-COVID levels. First-time buyer demand is set to weaken further over the rest of 2020 and into 2021.

The portal says that the remainder of 2020 and the start of 2021 are set to witness a reversal of the first-time buyer market dominance with a greater share of moves by existing home-owners who tend to move less often.

The search for space and the once in a lifetime re-valuation of what a home is worth in the wake of COVID means demand from existing homeowners shows no sign of weakening and remains 37% higher than pre-COVID levels and 53% higher than this time last year.

A large portion of existing home owners have either no mortgage or smaller loans, so affordability is less of a barrier to movement. This is especially true for households looking to trade out of cities to more rural areas with lower values and better value for money.

Existing owners are older – 75% of homeowners are over the age of 45 while over half of owners have no mortgage at all meaning 2021 could also give way to an increased volume of cash-only purchases.

The lockdown measures introduced in March unlocked latent demand for housing. Zoopla believes that a second spike in new cases, coupled with the Government’s recently announced tightening of restrictions, will support demand for housing in the near term. Those in a more secure financial position – such as homeowners with good levels of equity and little to no mortgage – will be galvanised into action.

N.B. A home mover in this context is defined as an existing homeowner

N.B. A home mover in this context is defined as an existing homeowner

On a regional basis, the relative strength of first-time buyer demand is not uniform. This reflects the underlying profile of buyers and the level of reliance on higher loan to value (LTV) mortgages, particularly at or above 90% LTV.

In 2019 around a fifth of all mortgages for home purchase were at this level. Reduced availability of mortgages at or over 90% LTV – as lenders meet increased demand at mid to lower LTVs – is a primary factor behind weakening demand.

Figures show that in September 2020 compared to Q1, demand amongst first-time buyers has grown the least in London (1.8%), Yorkshire and the Humber (+4.8%), and the North West (9.7%). By contrast, Scotland (+83.5%), the East (+66.2%) and the South East (+65.8%) have all registered the highest increases of demand amongst homeowners.

90% LTV lending is most accessible in housing markets with average or below average house prices where loan to income limits do not exclude a high proportion of prospective buyers. The strongest growth in recent years has been in regional markets outside of southern England, and Zoopla expects first-time buyer demand to be more affected here.

London, as ever, tells its own unique story. As a higher priced market, 90% LTV lending is limited to those on high incomes or those with larger deposits – signalling a new subset of affluent first-time buyer. But as the figures show, London is not immune to the effects of reduced LTV lending. Weaker first-time buyer demand in London will also reflect that more first-time buyers are looking outside the capital for their first home – factoring in less commuting and more flexibility in working from home – and moreover, most likely, the need for a smaller deposit.

As the market continues its recovery following the impact of COVID-19 and the 50 day market closure in England, the strength of demand has seen new sales agreed outperforming the same period in 2019 by +3%. However, it’s unlikely that 2020 will recover the sales lost to the market hiatus due to the three to four month lag time between sales agreed and legal completions and, ultimately, the portal expect sales to run 15% below 2019 levels by the year end.

Looking to next year, with demand currently tracking at 39% above this same period last year, the first quarter of 2021 is expected to deliver a windfall for the market, as sales agreed reach completion, and mortgage lenders and conveyancers make headway with the unprecedented backlog of applications.

Furthermore, the uptick in buyers is releasing more stock into the market and sales inventory is 10% above levels of availability 12 months prior. Greater supply increases choice, diluting competition for stock and regulating rate of house price growth.

House prices growth continues on an upward annual trajectory of +2.6% as demand outpaces supply. At a region and country level, the annual rate of growth ranges from +1.7% in the North East to +3.3% in the North West, Yorkshire and the Humber, and Wales. Nottingham and Manchester and recording price inflation of over 4% per annum.

Richard Donnell, Research and Insight Director, Zoopla, said: “Housing market conditions remain strong as new restrictions are introduced to control the spread of COVID. These changes are likely to continue to support housing demand in the near term as the importance of the home grows. However, the housing market will not remain immune to the impacts of weaker economic growth and rising unemployment.

“A change in the mix of buyers is supporting market conditions with sustained demand from equity rich existing owners seeking more space and a change in location. In contrast, first-time buyer demand is weakening. FTBs have been a driving force of housing sales over the last decade. They remain a key buyer group but lower availability of higher loan to value mortgages and increased movement by existing home-owners means a shift in the mix of home buyers into 2021.”